The intersection of a couple of recent events sent us into our DrinkTell™ database this week to do some research. Constellation Brands shares spiked 6% last Thursday as first quarter earnings surged past forecasts and the full year guidance was lifted. The beer division, Constellation Beer, reported net sales up 8% and depletions up 11.6%. Beer operating income was up a whopping 22%. The only sign of a possible cloud was an $87 million impairment charge taken against Ballast Point trademarks. For non-accountants (like us) an impairment charge is taken when estimated future cash flow of an asset is less than the book value of the asset. In short, the balance sheet goodwill of the trademarks was sliding with weaker than expected performance of the portfolio.

Our interest, however, was not Constellation Beer per se. The intersecting event here is that we had just put 2016 domestic beer volumes into DrinkTell™. Needless to say, we've all been talking for almost a half dozen years—more in some instances—about the strategic acquisition of some of the most highly regarded and highly successful craft brewers by mainline brand marketers.

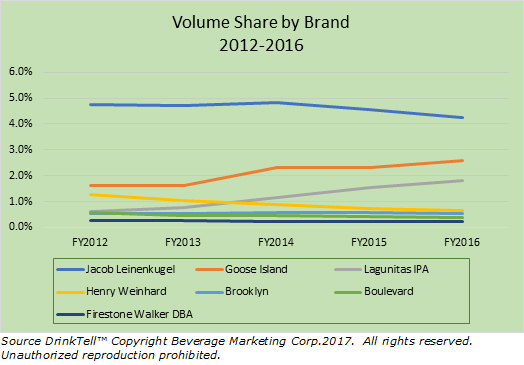

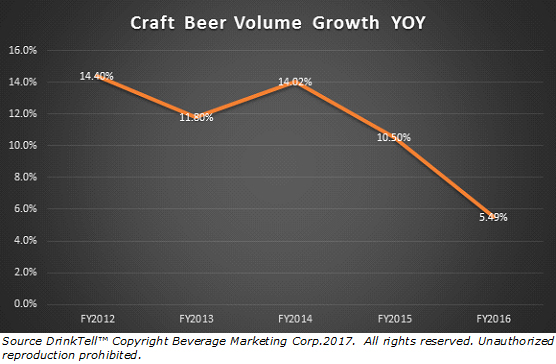

Tastes change over time, of course, and successful marketers give consumers what they want. Large brewers as well as small have been striving to do just that. So, our initial curiosity revolved around the question of how do acquired brands compare to the whole craft universe. In other words, share. The periods before and after acquisition in the infographic are not comparable. So, we don't have a measure of the acquirers' management performance as much as of the inherent quality or attractiveness of the acquired brands to consumers. Craft beer volume grew 70% from 11.3 to 19.2 million barrels since 2011. So, any brand that came close to holding most of its share in this expanding universe did well indeed. Here are some of the acquired brands. In this chart lines that are almost flat—or better—are "winners." |

That has changed. But now DrinkTell™ and other researchers tell us craft growth is slowing. It's six years since A-B purchased Goose Island, which seemed to be sort of a watershed. In 2014 Spanish brewer Mahou San Miguel bought 30% of Founders. Two years ago Duvel Moortgang acquired Firestone Walker, having already acquired Ommegang and Boulevard Brewing. Last fall Kirin bought a 24.5% stake in Brooklyn Brewery. Heineken NV recently completed its purchase of Lagunitas.

What's next? Are more similar acquisitions to come—or another approach? The markets, as well as private investors, demand endless growth. They are ardent suitors but fickle mates. Hockey great Wayne Gretzky used to have a facile answer to such challenges, "Skate to where the puck is going to be, not where it has been." Good luck with that, of course, unless you're Wayne Gretzky. Actually, one near term answer does seem to be the consolidation of brands among a diminishing number of owners.

The U.S. beer market is immense. As noted, we put 2016 domestic consumption at 19.2 million barrels. Analyzing and understanding such a market requires a commensurate volume of data—data like that found in DrinkTell™ or a comparable resource. For questions about this discussion or to look at our DrinkTell™ database yourself just give us a call. To order a BMC's U.S. Wine, Beer, or Spirits Guide, 2017 edition, just click below. |