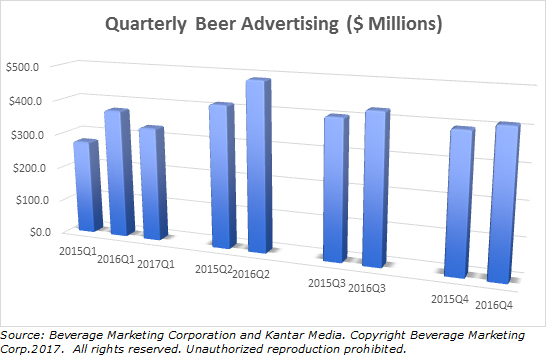

A couple of days ago a detailed report from Citigroup analyst Wendy Nicholson on first quarter U.S. Beer, Wine and Spirits advertising appeared to signal market caution. Nicholson's report led with the note that overall ad spending for the beverage alcohol category was down 6% year over year. That is pretty much what we see in our own DrinkTell™ data supplied quarterly by Kantar Media.

The analyst report covered the relevant topline detail before moving on to look at the specific marketers that Nicholson covers. Most of the year over year spending slide came from beer although vodka was also off, she said. The rest of the spirits categories were reported to have more modest ups and downs.

In the published report that we saw, Nicholson concluded that the critical point of analysis had to be sought in relative market share trends. We decided to follow this thought into DrinkTell™. We started by looking at two years of YOY rather than one. The underlying data raises some questions of its own. Beer did take a tumble but it had also had an astounding gain from first quarter 2015 to first quarter 2016—$276 million to $376 million. That's 36%. First quarter 2017 beer advertising was still almost 21% ahead of spending for first quarter 2015. |