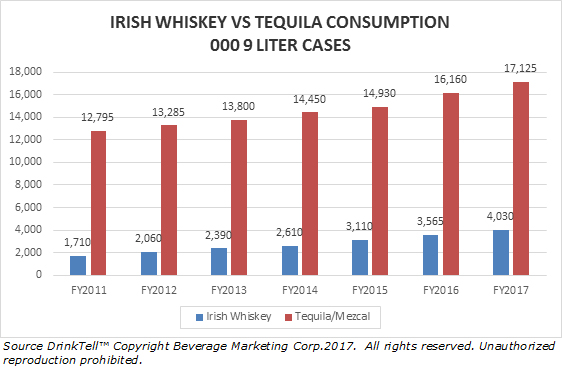

Both spirits command attractive retail case prices. We project the 2017 9-liter retail case price for Irish Whiskey to be $335. For Tequila/Mezcal we project $310. As with consumption, Tequila/Mezcal will represent a far larger market, $5.3 billion dollars versus $1.4 billion.

We know the popular Casamigos labels are probably kicking tail on the average case sale, retailing for about $480/case. So, there is money to be made in every tier—but is there a conclusion to the original question? We've put the best "case" and it looks like a long road to an ROI. It boils down to this. Industry sources claim 120,000 cases of Casamigos sold last year and are projecting 170,000 this year. If the supplier gross margin on a case is a whopping $160, then 170,000 cases shipped and paid for equal $27.2 million. That sounds like a 25-year payback.

We don't think that's what Diageo is thinking. Shareholders like Nick Train certainly hope not. We think that the bet that the British wizards just put down is that they will be able to out-market competitors and maintain growth in a very high return U.S. market (as well as leverage their strength in markets outside the U.S.)

Right or wrong, we're pretty sure that hard total market data like that found in the DrinkTell™ database was consulted long before contracts were ever considered. If you want to see how you can follow the money in DrinkTell™ or you have other questions about this column, please give us a call. To order a BMC U.S. Wine, Beer, or Spirits Guide, 2017 edition, just click below. |